Home » BUSINESS (Page 10)

Category Archives: BUSINESS

Starting a New Business

Anyone starting a new business this summer should be aware of their federal tax responsibilities.

Here are the top seven things the IRS wants you to know if you plan on opening a new business this year.

first, you must decide what type of business entity you are going to establish. The type your business takes will determine which tax form you have to file. The most common types of business are the sole proprietorship, partnership, corporation and S corporation.

The type of business you operate determines what taxes you must pay and how you pay them. The four general types of business taxes are income tax, self-employment tax, employment tax and excise tax.

An Employer Identification Number is used to identify a business entity. Generally, businesses need an EIN. Visit IRS.gov for more information about whether you will need an EIN. You can also apply for an EIN online at IRS.gov.

Good records will help you ensure successful operation of your new business. You may choose any recordkeeping system suited to your business that clearly shows your income and expenses. Except in a few cases, the law does not require any special kind of records. However, the business you are in affects the type of records you need to keep for federal tax purposes.

Every business taxpayer must figure taxable income on an annual accounting period called a tax year. The calendar year and the fiscal year are the most common tax years used.

Each taxpayer must also use a consistent accounting method, which is a set of rules for determining when to report income and expenses. The most commonly used accounting methods are the cash method and an accrual method. Under the cash method, you generally report income in the tax year you receive it and deduct expenses in the tax year you pay them. Under an accrual method, you generally report income in the tax year you earn it and deduct expenses in the tax year you incur them.

Visit the Business section of IRS.gov for resources to assist entrepreneurs with starting and operating a new business.

Links:

Starting A Business

Operating A Business

Closing A Business

Publication 4591, Small Business Federal Tax Responsibilities (PDF 470.1K)

Publication 334, Tax Guide for Small Business (PDF 286.2K)

Order Publication 1066C, A Virtual Small Business Tax Workshop DVD

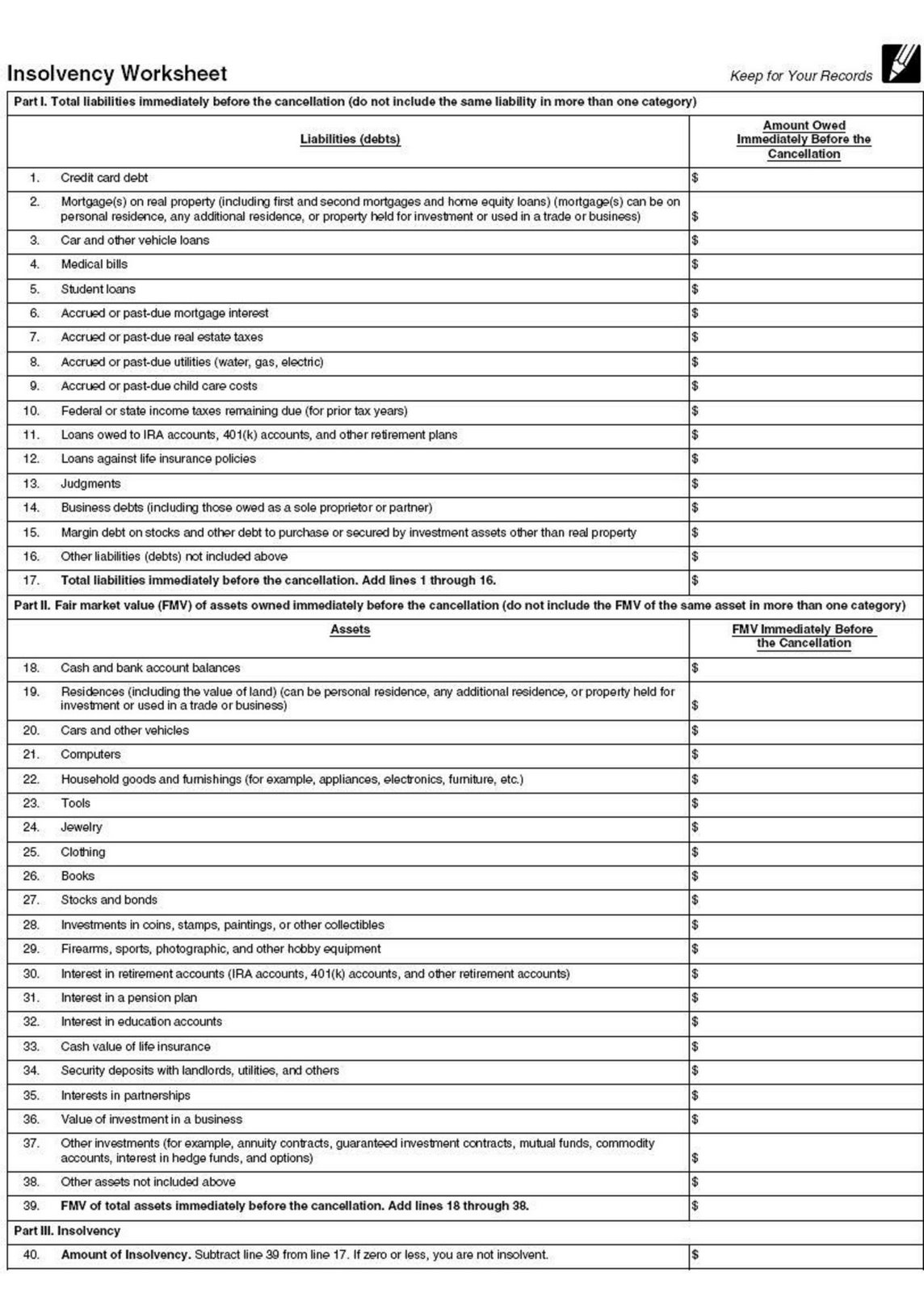

Canceled Debts, Foreclosures, Repossessions, and Abandonments

Insolvency

If you have qualified real property business indebtedness that is cancelled, you can elect to exclude this from income. However, the debt must meet the following criteria:

1) It must be incurred or assumed in connection with real property used in a trade or business.

2) It must be secured by such real property.

3) It must be incurred or assumed at either of the following times:

a. Before 1993

b. After 1992, if the debt is either (i) qualified acquisition indebtedness (defined below), or (ii) debt incurred to refinance qualified real property business debt incurred or assumed before 1993 ( but only to the extend the amount of such debt does not exceed the amount of debt being refinanced.)

4) It must be debt to which you elect to apply these rules

Qualified principal Residence indebtedness

What’s new for 2008

The qualified principle residence indebtedness exclusion has been extended. The extension includes debts discharged after 2006 and before 2013.