By Stacie Clifford Kitts, CPA

Generally

Generally, if you have a debt (that is a debt that you are personally liable for) that is cancelled or forgiven, you must include the amount of cancelled debt as ordinary income on your income tax return. However, there are exceptions to this rule. Here is a list of some of the exceptions which would allow you to exclude the cancelled debt from income:

1) If the cancellation is intended to be a gift, then you are not required to report it as income. See Publication 525 for more information.

2) Certain student loans, if they contain a provision that the debt can be cancelled if certain qualifications are met.

3) If payments on the debt would have been considered tax deductions at the time the principal payments were made.

4) If the price of an item you have purchased on credit is reduced by the seller at a time when you are insolvent. However, you must reduce your basis in the property by the amount of the reduction.

There are also certain situation which allow you to exclude debt cancelation from income.

Bankruptcy

If you are bankrupt and you file for bankruptcy under title 11, the debt that is cancelled is not included in your income. But only if the cancellation of debt is under the jurisdiction of a court and the court approves the cancelation.

If your debt is cancelled, you should complete and attach

Form 982 to your federal income tax return.

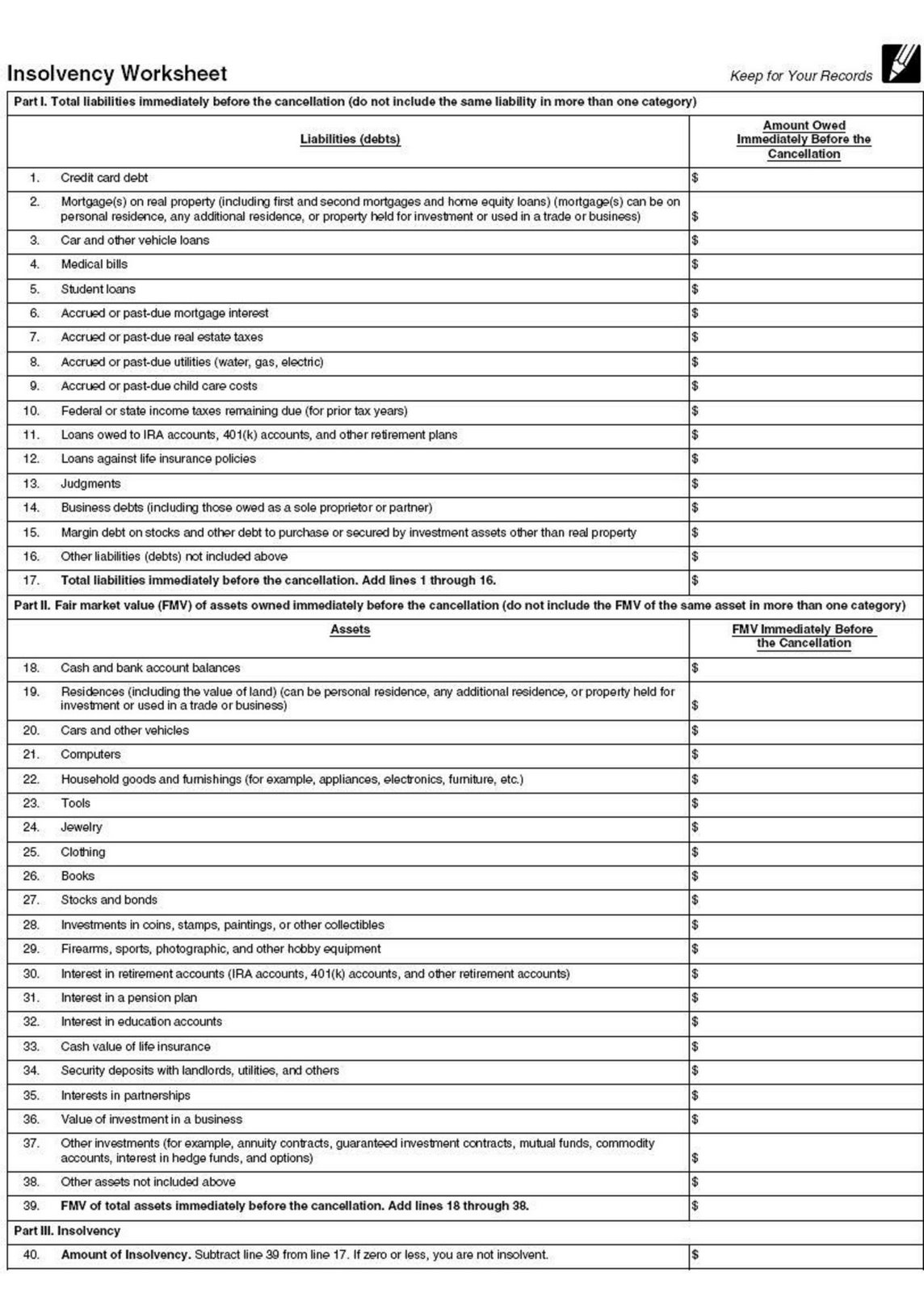

Insolvency

You are not required to include debt cancellation to the extent that you are insolvent immediately before the cancellation. You are insolvent if the total of your liabilities, exceeds the FMV of all of your assets.

To show that you are insolvent and to exclude cancelled debt, attach

Form 982 to your income tax return.

The following worksheet can be used to calculate the extent that you were insolvent.

[Click on the picture to enlarge]

Certain qualified farm indebtedness can be excluded from income – See publication 4681

Qualified Real Property Business Indebtedness

If you have qualified real property business indebtedness that is cancelled, you can elect to exclude this from income. However, the debt must meet the following criteria:

1) It must be incurred or assumed in connection with real property used in a trade or business.

2) It must be secured by such real property.

3) It must be incurred or assumed at either of the following times:

a. Before 1993

b. After 1992, if the debt is either (i) qualified acquisition indebtedness (defined below), or (ii) debt incurred to refinance qualified real property business debt incurred or assumed before 1993 ( but only to the extend the amount of such debt does not exceed the amount of debt being refinanced.)

4) It must be debt to which you elect to apply these rules

Qualified principal Residence indebtedness

The qualified debt from your principal residence can be excluded from income if it is cancelled. The maximum amount that can be excluded is $2 million ($1 million if you are married filing separately).

Be sure to check out

Publication 4681 for a definition of qualified principal residence indebtedness.

Attach a completed

Form 982 to your federal income tax return to exclude the income.

Qualified Midwestern Disaster Area Indebtedness

If non business debt is cancelled by an applicable entity and you are a qualified individual you can exclude the cancelation from income. See publication 4681 for more details.

What’s new for 2008

The qualified principle residence indebtedness exclusion has been extended. The extension includes debts discharged after 2006 and before 2013.

The Heartland Disaster Tax Act Relief of 2008 which allows qualified individual to exclude from gross income discharges of certain indebtedness because of Midwestern Disasters.

The American Recovery and Reinvestment Act of 2009 allows certain businesses to make an elect to defer over a five year period the recognition of income from the cancellation of business debt arising from the reacquisition of certain types of business debt repurchased in 2009 or 2010. However, for the current or subsequent years, if you make the election to defer over the five year period, you cannot exclude the cancellation of debt related to a title 11 bankruptcy case, insolvency, qualified farm indebtedness or qualified real property business indebtedness. See Section 108(i) for more information.