The Mortgage Forgiveness Debt Relief Act of 2007 generally allows taxpayers to exclude income from the discharge of debt on their principal residence. Debt reduced through mortgage restructuring, as well as mortgage debt forgiven in connection with a foreclosure, qualify for this relief.

This provision applies to debt forgiven in calendar years 2007 through 2012. Up to $2 million of forgiven debt is eligible for this exclusion ($1 million if married filing separately). The exclusion doesn’t apply if the discharge is due to services performed for the lender or any other reason not directly related to a decline in the home’s value or the taxpayer’s financial condition.

The questions and answers, below, are based on the law prior to the passage of the Mortgage Forgiveness Debt Relief Act of 2007.

1. What is Cancellation of Debt?

If you borrow money from a commercial lender and the lender later cancels or forgives the debt, you may have to include the cancelled amount in income for tax purposes, depending on the circumstances. When you borrowed the money you were not required to include the loan proceeds in income because you had an obligation to repay the lender. When that obligation is subsequently forgiven, the amount you received as loan proceeds is reportable as income because you no longer have an obligation to repay the lender. The lender is usually required to report the amount of the canceled debt to you and the IRS on a Form 1099-C, Cancellation of Debt.

Here’s a very simplified example. You borrow $10,000 and default on the loan after paying back $2,000. If the lender is unable to collect the remaining debt from you, there is a cancellation of debt of $8,000, which generally is taxable income to you.

2. Is Cancellation of Debt income always taxable?

Not always. There are some exceptions. The most common situations when cancellation of debt income is not taxable involve:

Bankruptcy: Debts discharged through bankruptcy are not considered taxable income.

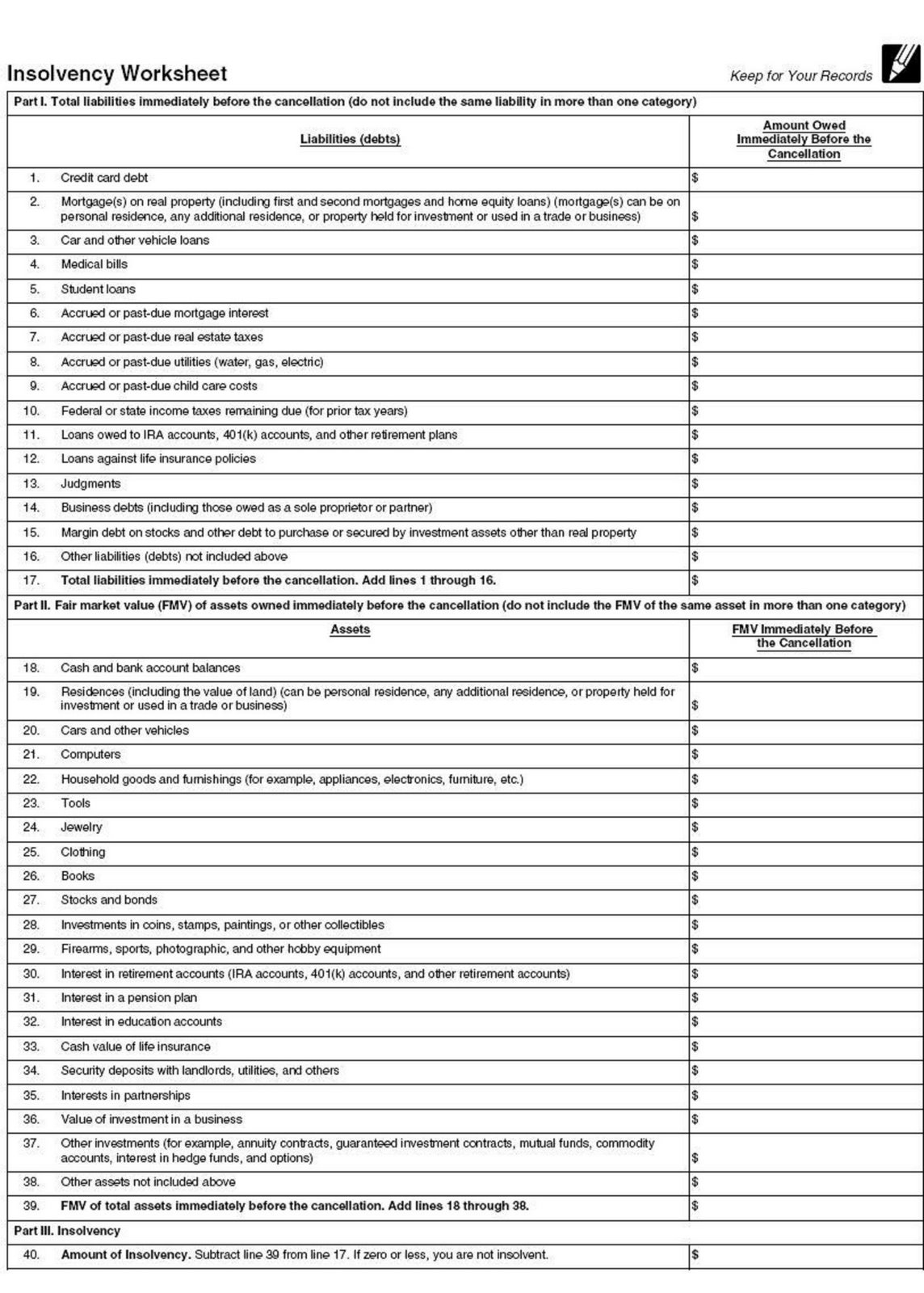

Insolvency: If you are insolvent when the debt is cancelled, some or all of the cancelled debt may not be taxable to you.You are insolvent when your total debts are more than the fair market value of your total assets.Insolvency can be fairly complex to determine and the assistance of a tax professional is recommended if you believe you qualify for this exception.

Certain farm debts:If you incurred the debt directly in operation of a farm, more than half your income from the prior three years was from farming, and the loan was owed to a person or agency regularly engaged in lending, your cancelled debt is generally not considered taxable income.The rules applicable to farmers are complex and the assistance of a tax professional is recommended if you believe you qualify for this exception.

Non-recourse loans:A non-recourse loan is a loan for which the lender’s only remedy in case of default is to repossess the property being financed or used as collateral.That is, the lender cannot pursue you personally in case of default.Forgiveness of a non-recourse loan resulting from a foreclosure does not result in cancellation of debt income.However, it may result in other tax consequences, as discussed in Question 3 below.

3. I lost my home through foreclosure. Are there tax consequences?

There are two possible consequences you must consider:

Taxable cancellation of debt income.(Note: As stated above, cancellation of debt income is not taxable in the case of non-recourse loans.)

A reportable gain from the disposition of the home (because foreclosures are treated like sales for tax purposes).(Note: Often some or all of the gain from the sale of a personal residence qualifies for exclusion from income.)

Use the following steps to compute the income to be reported from a foreclosure:

Step 1 – Figuring Cancellation of Debt Income (Note: For non-recourse loans, skip this section. You have no income from cancellation of debt.)

1. Enter the total amount of the debt immediately prior to the foreclosure.___________2. Enter the fair market value of the property from Form 1099-C, box 7. ___________3. Subtract line 2 from line 1.If less than zero, enter zero.___________

The amount on line 3 will generally equal the amount shown in box 2 of Form 1099-C. This amount is taxable unless you meet one of the exceptions in question 2. Enter it on line 21, Other Income, of your Form 1040.

Step 2 – Figuring Gain from Foreclosure4. Enter the fair market value of the property foreclosed.For non-recourse loans, enter the amount of the debt immediately prior to the foreclosure ________5. Enter your adjusted basis in the property.(Usually your purchase price plus the cost of any major improvements.) ____________6. Subtract line 5 from line 4. If less than zero, enter zero.

The amount on line 6 is your gain from the foreclosure of your home. If you have owned and used the home as your principal residence for periods totaling at least two years during the five year period ending on the date of the foreclosure, you may exclude up to $250,000 (up to $500,000 for married couples filing a joint return) from income. If you do not qualify for this exclusion, or your gain exceeds $250,000 ($500,000 for married couples filing a joint return), report the taxable amount on Schedule D, Capital Gains and Losses.

4. I lost money on the foreclosure of my home. Can I claim a loss on my tax return?

No. Losses from the sale or foreclosure of personal property are not deductible.

5. Can you provide examples?

A borrower bought a home in August 2005 and lived in it until it was taken through foreclosure in September 2007. The original purchase price was $170,000, the home is worth $200,000 at foreclosure, and the mortgage debt canceled at foreclosure is $220,000. At the time of the foreclosure, the borrower is insolvent, with liabilities (mortgage, credit cards, car loans and other debts) totaling $250,000 and assets totaling $230,000.

The borrower figures income from the foreclosure as follows:

Use the following steps to compute the income to be reported from a foreclosure:

Step 1 – Figuring Cancellation of Debt Income (Note: For non-recourse loans, skip this section. You have no income from cancellation of debt.)

1. Enter the total amount of the debt immediately prior to the foreclosure.___$220,000__2. Enter the fair market value of the property from Form 1099-C, box 7. ___$200,000__3. Subtract line 2 from line 1.If less than zero, enter zero.___$20,000__

The amount on line 3 will generally equal the amount shown in box 2 of Form 1099-C. This amount is taxable unless you meet one of the exceptions in question 2. Enter it on line 21, Other Income, of your Form 1040.

Step 2 – Figuring Gain from Foreclosure

4. Enter the fair market value of the property foreclosed.For non-recourse loans, enter the amount of the debt immediately prior to the foreclosure. __$200,000__5. Enter your adjusted basis in the property.(Usually your purchase price plus the cost of any major improvements.) ___$170,000__6. Subtract line 5 from line 4.If less than zero, enter zero.___$30,000__

The amount on line 6 is your gain from the foreclosure of your home. If you have owned and used the home as your principal residence for periods totaling at least two years during the five year period ending on the date of the foreclosure, you may exclude up to $250,000 (up to $500,000 for married couples filing a joint return) from income. If you do not qualify for this exclusion, or your gain exceeds $250,000 ($500,000 for married couples filing a joint return), report the taxable amount on Schedule D, Capital Gains and Losses.

In this situation, the borrower has a tax-free home-sale gain of $30,000 ($200,000 minus $170,000), because they owned and lived in their home as a principal residence for at least two years. Ordinarily, the borrower would also have taxable debt-forgiveness income of $20,000 ($220,000 minus $200,000). But since the borrower’s liabilities exceed assets by $20,000 ($250,000 minus $230,000) there is no tax on the canceled debt.

Other examples can be found in IRS Publication 544, Sales and Other Dispositions of Assets, under the section “Foreclosures and Repossessions”.

6. I don’t agree with the information on the Form 1099-C. What should I do?

Contact the lender. The lender should issue a corrected form if the information is determined to be incorrect. Retain all records related to the purchase of your home and all related debt.

7. I received a notice from the IRS on this. What should I do?

The IRS urges borrowers with questions to call the phone number shown on the notice. The IRS also urges borrowers who wind up owing additional tax and are unable to pay it in full to use the installment agreement form, normally included with the notice, to request a payment agreement with the agency.

8. Where else can I go to get tax help?

If you are having difficulty resolving a tax problem (such as one involving an IRS bill, letter or notice) through normal IRS channels, the

Taxpayer Advocate Service may be able to help. For more information, you can also call the TAS toll-free case intake line at 1-877-777-4778, TTY/TDD 1-800-829-4059.

In some cases, you may qualify for free or low-cost assistance from a Low Income Taxpayer Clinic (LITC). LITCs are independent organizations that represent low income taxpayers in tax disputes with the IRS. Find

information on an LITCs in your area.

Related Items:

Publication 523, Selling Your Home

Publication 544, Sales and Other Dispositions of Assets

Publication 908, Bankruptcy Tax Guide

Form 1040, U.S. Individual Income Tax Return

Form 1040, Schedule D, Capital Gains and Losses

Form 1099-C, Cancellation of Debt

Form 9465, Installment Agreement Request

{kind=link}