How to Keep Good Records

More IRS Summer Tax Tips

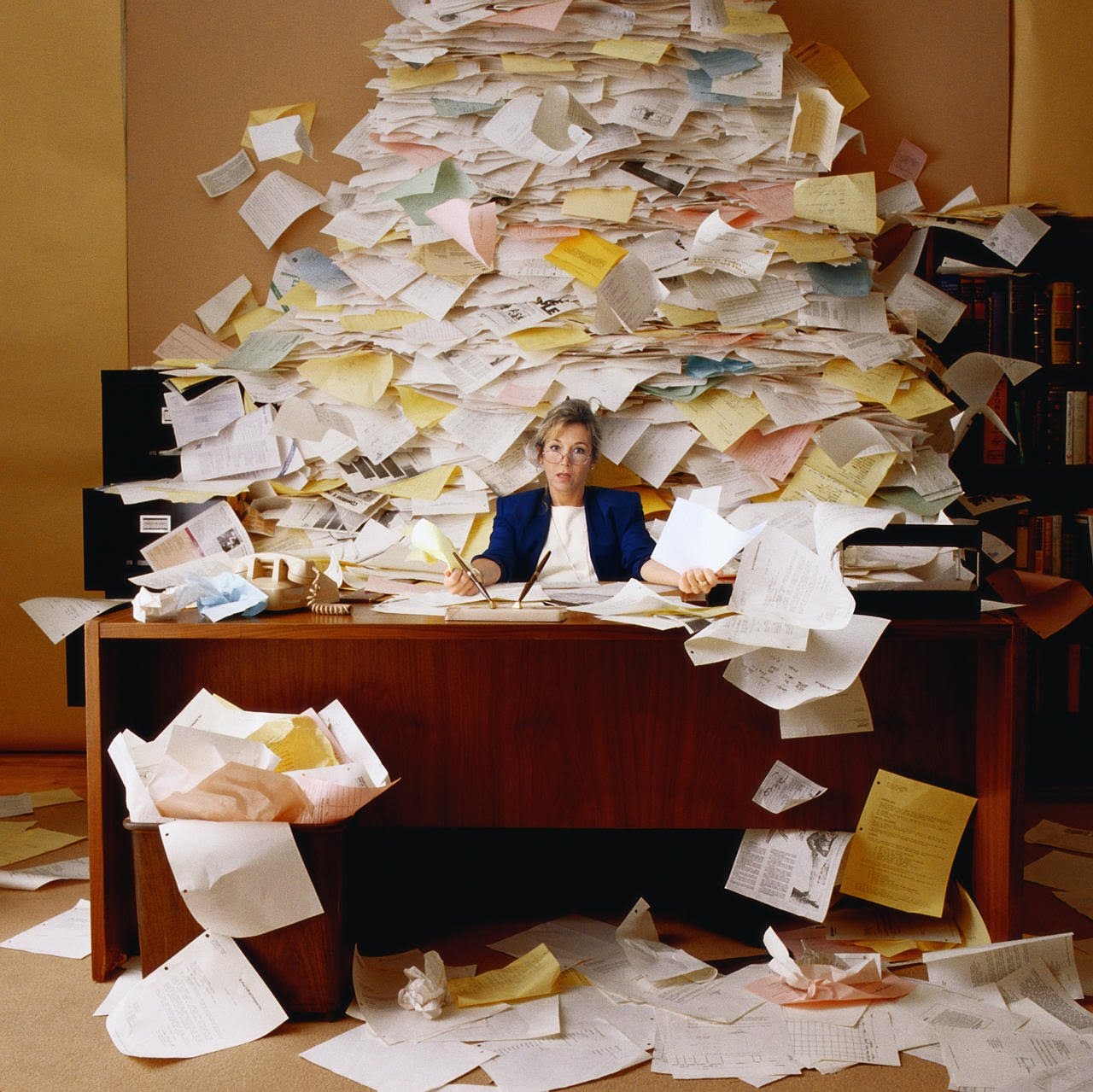

Although most people won’t be filing their tax returns for several months, the dog days of summer are actually a great time to start planning for the tax filing season by ensuring your records are organized. Whether you are an individual taxpayer or a business owner, you can avoid headaches at tax time with good records because they will help you remember transactions you made during the year.

Here are a few things the IRS wants you to know about recordkeeping.

Keeping well-organized records also ensures you can answer questions if your return is selected for examination or prepare a response if you are billed for additional tax. In most cases, the IRS does not require you to keep records in any special manner. Generally speaking, you should keep any and all documents that may have an impact on your federal tax return.

Individual taxpayers should usually keep the following records supporting items on their tax returns for at least three years:

Bills

Credit card and other receipts

Invoices

Mileage logs

Canceled, imaged or substitute checks or any other proof of payment

Any other records to support deductions or credits you claim on your return

You should normally keep records relating to property until at least three years after you sell or otherwise dispose of the property. Examples include:

A home purchase or improvement

Stocks and other investments

Individual Retirement Arrangement transactions

Rental property records

If you are a small business owner, you must keep all your employment tax records for at least four years after the tax becomes due or is paid, whichever is later. Examples of important documents business owners should keep Include:

Gross receipts: Cash register tapes, bank deposit slips, receipt books, invoices, credit card charge slips and Forms 1099-MISC

Proof of purchases: Canceled checks, cash register tape receipts, credit card sales slips and invoices

Expense documents: Canceled checks, cash register tapes, account statements, credit card sales slips, invoices and petty cash slips for small cash payments

Documents to verify your assets: Purchase and sales invoices, real estate closing statements and canceled checks

For more information about recordkeeping, check out IRS Publications 552, Recordkeeping for Individuals, 583, Starting a Business and Keeping Records, and Publication 463, Travel, Entertainment, Gift, and Car Expenses. These publications are available on the IRS Web site, IRS.gov or by calling 800-TAX-FORM (800-829-3676).

Links:

IRS Publication 552, Recordkeeping for Individuals (PDF)

IRS Publication 583, Starting a Business and Keeping Records (PDF)

IRS Publication 463, Travel, Entertainment, Gift, and Car Expenses (PDF)

Your Tax Preparer Should Prove She (or He) Has-a-Clue Before Preparing Your Tax Return

By Stacie Clifford Kitts, CPA

The Wandering Tax Pro (aka Robert D Flach) has a great post that you should check out. In After thoughts Part I, Robert sings the praises of the Vita program while addressing a prior post centered on whether tax preparers should be registered and licensed. I actually have some strong feelings about the topic, so I am going to jump right into it.

Here is a little background for those readers who may not be familiar with the debate: The IRS is seeking proposals on how to advance tax preparer performance by implementing consistent standards. You can read more about this over at The Business Perspective.

So on with my argument: I have picked up many returns where I wished that the preparer had been required to take a proficiency test prior to touching the tax forms.

Case in point, how about a partnership return (Form 1065) prepared by an attorney for a single member LLC. The client and the attorney were actually perplexed as to why the IRS was sending out “what the heck are you doing letters.”

Alternatively, how about the Enrolled Agent who filed a first year C Corporation return (Form 1120) for an LLC because she thought LLC meant Limited liability Corporation.

No kidding!

Yes, I have to say, I think it is a good idea to require tax preparers to prove their competency before they are allowed to charge a fee for the preparation of a tax return. Although I believe the proposed regulations are targeted more toward persons who are not CPAs, lawyers, or EA’s, it is obvious from what I have described that a proficiency test is needed for everyone preparing tax returns.

As a CPA, I am familiar with regulation, as I am required to keep my license up to date by taking 80 hours of continuing education every two years. I have no problem with taking a proficiency exam. If I am unable to pass it, well then I should not be preparing tax returns. The tax profession is not stagnate; laws are constantly changing. Just because someone could accurately prepare a return last year, does not mean he or she understands the rules this year.

And, for those prepares out there who are not familiar with the federal filing requirements of an LLC, here are some clues: Unless you elect to be taxed differently under the check the box rules by filing Form 8832 Entity Classification Election, owners of single member LLC’s file a schedule C along with their individual income tax return Form 1040. LLC’s with two or more member file a partnership return Form 1065.